Insurance Planning as a Wealth Management Strategy

Insurance planning plays a pivotal role in comprehensive wealth management. It provides a safety net to protect assets, income, and overall financial well-being by mitigating financial risks and safeguarding against unforeseen events.

Insurance policies, such as life insurance, health insurance, and property insurance, serve as financial cushions that can cover expenses or provide income replacement in the event of death, illness, disability, or property damage. By planning for potential risks, individuals can minimize the financial impact of these events and preserve their wealth.

Role of Insurance in Wealth Management

- Protecting Assets: Insurance policies can safeguard valuable assets like homes, cars, and businesses from unexpected events such as fire, theft, or natural disasters.

- Income Replacement: Life insurance and disability insurance provide income protection in case of death or disability, ensuring financial stability for dependents and beneficiaries.

- Risk Mitigation: Insurance plans mitigate financial risks by spreading the cost of potential losses over a larger group of policyholders, minimizing the burden on individuals.

Types of Insurance for Wealth Management

Insurance plays a vital role in wealth management by providing financial protection against unforeseen events. Understanding the different types of insurance policies and their coverage can help individuals make informed decisions when planning their wealth management strategies.

Life Insurance

Life insurance provides financial security for beneficiaries in the event of the policyholder’s death. It can ensure that loved ones receive a lump sum payout, which can cover expenses such as funeral costs, outstanding debts, and future financial needs. There are two main types of life insurance: term life insurance, which provides coverage for a specific period, and whole life insurance, which provides coverage for the policyholder’s entire life.

Disability Insurance

Disability insurance provides income replacement if an individual becomes unable to work due to an illness or injury. It can help cover expenses such as mortgage payments, living expenses, and medical bills. Disability insurance can be especially important for individuals who rely on their income to maintain their lifestyle and financial commitments.

Health Insurance

Health insurance covers medical expenses, including hospital stays, doctor visits, and prescription drugs. It can provide peace of mind by ensuring that individuals have access to quality healthcare without facing financial hardship. Health insurance policies vary in terms of coverage and premiums, so it’s important to choose a plan that meets specific needs and budget.

Property Insurance

Property insurance protects homes, vehicles, and other assets from damage or loss due to events such as fire, theft, or natural disasters. It can provide financial compensation to cover repair or replacement costs, helping individuals recover from unexpected events and preserve their wealth.

Factors to Consider When Selecting Insurance Policies

When selecting insurance policies for a wealth management plan, individuals should consider the following factors:

– Age and health

– Income and financial obligations

– Assets and investments

– Risk tolerance

– Long-term financial goals

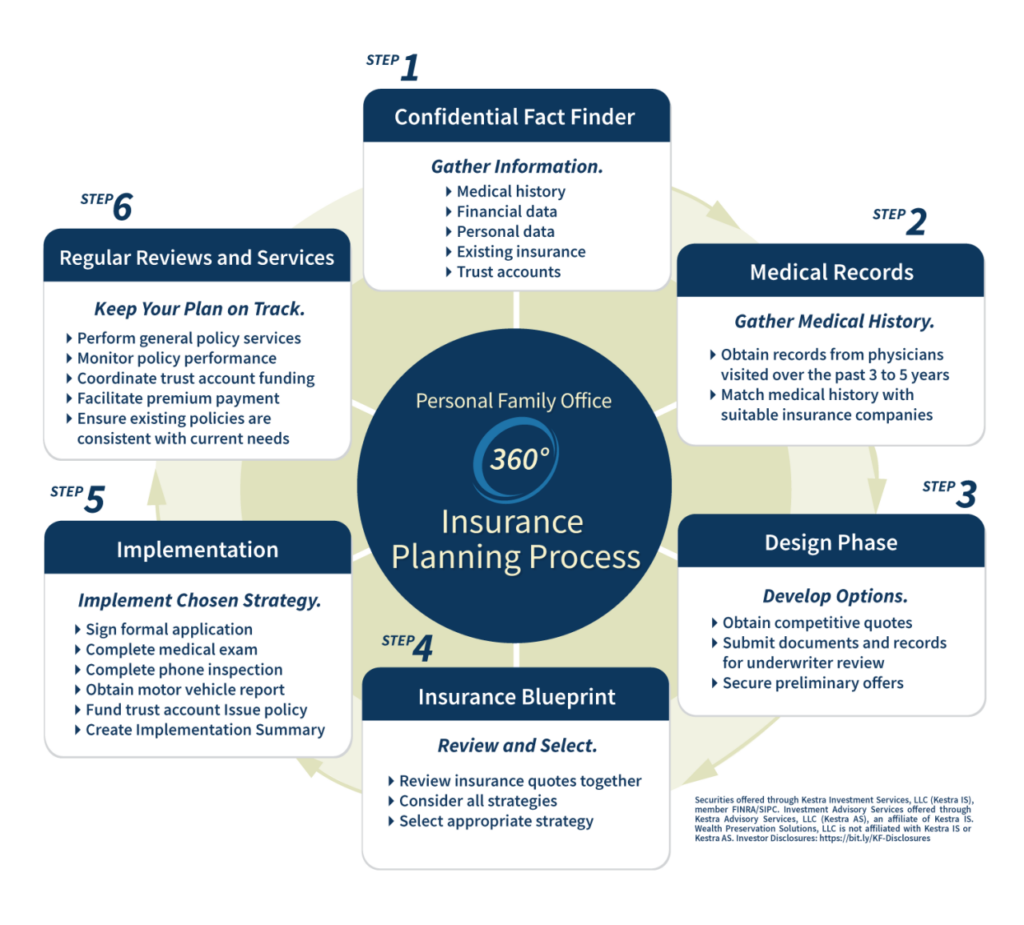

Integrating Insurance into Wealth Management Plans

Integrating insurance into wealth management plans involves a strategic approach that aligns insurance coverage with overall investment objectives and financial goals. It considers the unique needs and risk tolerance of each client, ensuring that insurance serves as a complementary tool to enhance portfolio performance and preserve wealth.

Insurance planning should align with investment strategies, providing a safety net against potential financial risks. By identifying and mitigating potential liabilities, insurance can help protect assets, secure future income streams, and preserve wealth for future generations.

Risk Assessment and Insurance Coverage

Integrating insurance into wealth management plans begins with a thorough risk assessment. This involves identifying potential risks that could impact financial security, such as premature death, disability, or unexpected medical expenses. Based on the risk assessment, appropriate insurance coverage can be recommended to mitigate these risks and protect the client’s financial well-being.

Types of Insurance for Wealth Management

A range of insurance products can be used in wealth management plans, including life insurance, disability insurance, long-term care insurance, and health insurance. Each type of insurance provides specific protection against different risks, ensuring that the client’s financial security is well-rounded.

Benefits of Insurance in Wealth Management

- Preservation of Wealth: Insurance can help preserve wealth by providing financial protection against unexpected events that could deplete assets.

- Income Protection: Disability insurance and life insurance can provide income protection, ensuring that financial obligations can be met even if the client is unable to work or passes away.

- Estate Planning: Life insurance can be used as an estate planning tool to ensure that assets are distributed according to the client’s wishes.

- Tax Benefits: Certain types of insurance, such as life insurance and long-term care insurance, offer tax benefits that can further enhance the client’s financial well-being.

Tax Considerations in Insurance Planning

Tax considerations play a crucial role in wealth management strategies involving insurance policies. Understanding the tax implications of various insurance products is essential for optimizing wealth accumulation and distribution while minimizing tax liabilities.

Life Insurance

Life insurance policies provide a tax-advantaged means of accumulating wealth. Premiums paid towards life insurance are often tax-deductible, reducing the taxable income of the policyholder. Moreover, the death benefit received by the beneficiaries is generally tax-free, providing a substantial financial cushion for loved ones without triggering any tax obligations.

Annuities

Annuities offer another tax-efficient wealth accumulation option. Contributions made towards an annuity are typically tax-deferred, meaning that taxes are not paid until withdrawals are made. When withdrawals are taken, they are taxed as ordinary income, but the tax burden is spread over the lifetime of the annuitant, potentially resulting in lower overall tax liability.

Strategies for Optimizing Coverage

To optimize insurance coverage while minimizing tax liabilities, consider the following strategies:

- Maximize tax-deductible premiums by contributing to qualified retirement plans and life insurance policies.

- Consider purchasing life insurance policies with a cash value component, which grows tax-deferred and can be accessed through loans or withdrawals.

- Utilize annuities to defer and spread out tax payments on accumulated savings.

li>Coordinate insurance policies with other estate planning tools, such as trusts and wills, to ensure a comprehensive and tax-efficient distribution of assets.

By carefully considering the tax implications of insurance policies, wealth managers can help clients achieve their financial goals while minimizing their tax burden.

Legal and Regulatory Aspects of Insurance Planning

Insurance planning in wealth management is governed by a comprehensive legal and regulatory framework designed to protect consumers and ensure the integrity of the insurance industry. Understanding these regulations is crucial for financial advisors and wealth managers to ensure compliance and provide ethical and responsible advice to their clients.

Role of Insurance Brokers, Financial Advisors, and Attorneys

Insurance brokers and financial advisors play a vital role in ensuring compliance with insurance regulations. They are required to be licensed and have a thorough understanding of the legal and regulatory environment governing insurance products. Insurance brokers act as intermediaries between clients and insurance companies, helping clients navigate the complex insurance market and secure the most appropriate coverage. Financial advisors, on the other hand, provide comprehensive wealth management services, including insurance planning. They work closely with insurance brokers to ensure that clients’ insurance needs are aligned with their overall financial goals and objectives.

Attorneys also play a significant role in insurance planning. They can provide legal advice on insurance contracts, assist with estate planning, and represent clients in insurance disputes. Attorneys can help ensure that insurance policies are drafted in a manner that protects the client’s interests and complies with applicable laws and regulations.

Case Studies and Examples

Insurance planning plays a crucial role in wealth management, as it offers protection, mitigates risks, and enhances financial outcomes. Let’s explore real-world case studies and examples to illustrate how insurance planning has been successfully implemented.

These case studies showcase how insurance products have protected wealth, provided financial security, and facilitated the achievement of financial goals. They also highlight the lessons learned and best practices that can guide effective insurance planning.

Case Study: Risk Mitigation and Wealth Preservation

A wealthy entrepreneur purchased a life insurance policy with a large death benefit. Upon their untimely passing, the policy provided a substantial payout to their family, ensuring their financial security and preserving their wealth.

This case study demonstrates the importance of life insurance in mitigating the financial impact of unexpected events. By ensuring that loved ones are financially protected in the event of the policyholder’s death, insurance planning safeguards wealth and provides peace of mind.

Case Study: Estate Planning and Tax Optimization

A high-net-worth individual used a life insurance trust to transfer assets to their beneficiaries while minimizing estate taxes. The trust was funded with a life insurance policy, which provided a tax-free death benefit to the beneficiaries.

This case study highlights the role of insurance planning in estate planning and tax optimization. By utilizing a life insurance trust, the individual was able to reduce the taxable value of their estate, ensuring that more of their wealth was passed on to their beneficiaries.