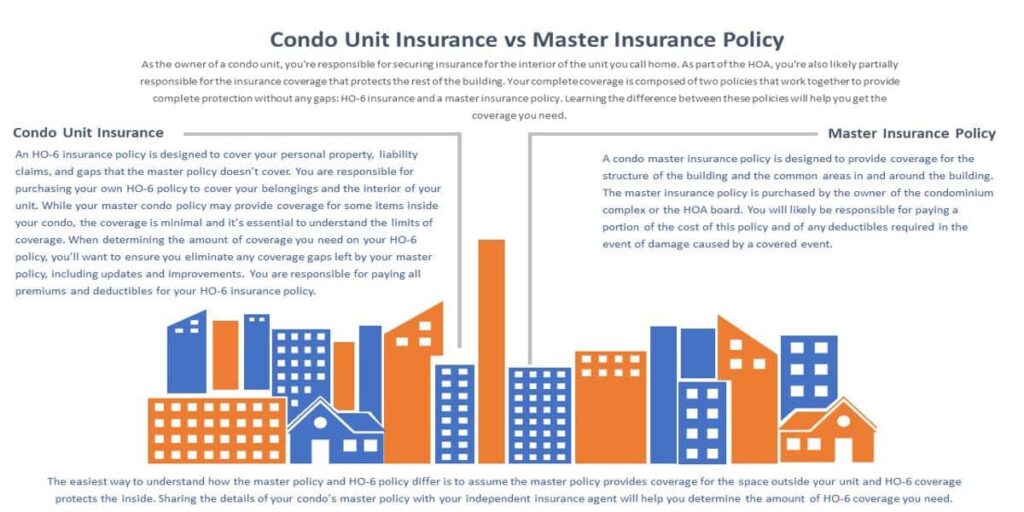

Coverage and Limitations

A condo association master insurance policy provides coverage for a wide range of potential risks faced by the association and its members. Understanding the specific coverages and limitations of the policy is essential for ensuring adequate protection.

The policy typically includes coverage for the following:

- Property damage to the common areas and individual units

- Liability for injuries or property damage caused by the association or its members

- Loss of income due to a covered event

- Special assessments for unexpected expenses

However, it is important to note that there are also certain exclusions and limitations to coverage. For example, the policy may not cover:

- Intentional acts or negligence by the association or its members

- Flooding or earthquake damage

- Personal property of individual unit owners

It is crucial for condo association members to carefully review the terms and conditions of the master insurance policy to ensure they understand the extent of their coverage and any potential gaps. This will help them make informed decisions about additional insurance policies or risk management measures.

Property Coverage

The master insurance policy covers the following types of property:

- Buildings

- Personal property

- Improvements and betterments

The policy determines the value of the property using one of the following methods:

- Actual cash value (ACV)

- Replacement cost value (RCV)

ACV is the current market value of the property, minus depreciation. RCV is the cost to replace the property with a new one of similar kind and quality. The policy will specify which method is used to determine the value of the property.

To file a claim for property damage, you should:

- Contact your insurance company as soon as possible.

- Provide the insurance company with a description of the damage.

- Submit a proof of loss form.

- Cooperate with the insurance company’s investigation.

The insurance company will then process your claim and determine whether you are entitled to benefits.

Liability Coverage

Liability coverage protects the condo association from financial responsibility for injuries or damages caused to others as a result of the association’s negligence or actions. This coverage is essential to safeguard the association and its members from potential lawsuits and financial losses.

Covered Liability Types

The master policy typically covers various types of liability, including:

- Bodily Injury Liability: Covers claims for injuries sustained by non-residents on the association’s property, such as guests, visitors, or contractors.

- Property Damage Liability: Covers claims for damage to property belonging to others, such as damage to neighboring units or common areas.

- Personal Injury Liability: Covers claims for non-physical injuries, such as defamation, false arrest, or malicious prosecution.

- Directors and Officers Liability: Covers claims against board members and officers for alleged wrongful acts or omissions in their capacity as association leaders.

Common Liability Claims

Common liability claims that may arise in a condo association include:

- Slips and falls on common areas, such as hallways, stairs, or parking lots

- Negligent maintenance of common areas, leading to property damage or injuries

- Defective conditions in the unit or common areas, causing injuries or property damage

- Acts or omissions of board members or officers, resulting in financial losses or reputational damage

Importance of Adequate Coverage

Maintaining adequate liability coverage is crucial for the following reasons:

- Financial Protection: Liability coverage provides a financial safety net to cover legal expenses, settlements, and judgments in the event of a lawsuit.

- Risk Mitigation: Adequate coverage helps mitigate the association’s exposure to financial risks and protects its assets from potential losses.

- Peace of Mind: Knowing that the association is adequately protected from liability claims provides peace of mind to board members and residents.

Special Assessments

Special assessments are additional charges levied on condo owners to cover unexpected or major expenses that cannot be covered by the regular operating budget. These assessments can be necessary for various reasons, such as major repairs, renovations, or legal expenses.

The process for approving and collecting special assessments typically involves the following steps:

Approval Process

- The condo association board identifies the need for a special assessment and determines the amount required.

- The board presents the proposal to the owners at a special meeting or through a written notice.

- The owners vote on the proposal, and if approved by the required majority, the assessment is authorized.

Collection Process

- The condo association sends out invoices to the owners for the special assessment.

- Owners are typically given a set period of time to pay the assessment.

- If an owner fails to pay the assessment, the association may take legal action to collect the debt.

Managing Special Assessments Effectively

Here are some tips for managing special assessments effectively:

- Communicate clearly with owners about the need for the assessment and how the funds will be used.

- Establish a clear and transparent process for approving and collecting special assessments.

- Consider offering payment plans or other financial assistance to owners who may have difficulty paying the assessment.

- Regularly review the condo association’s financial reserves to ensure that there are sufficient funds to cover potential future special assessments.

Insurance Premiums

Insurance premiums are calculated based on a variety of factors, including the type of coverage, the amount of coverage, and the risk associated with the property.

Factors that can affect the cost of premiums include:

- The type of construction of the building

- The age of the building

- The location of the building

- The claims history of the building

- The deductible amount

There are a number of things that condo associations can do to reduce their insurance premiums, including:

- Installing safety features, such as smoke detectors and fire sprinklers

- Maintaining the property in good condition

- Having a strong claims history

- Negotiating with insurance companies

Claims Process

Filing a claim under the master policy is a straightforward process. Here’s an overview of the steps involved:

When an incident occurs that may be covered under the master policy, it’s crucial to notify the insurance company promptly. This can be done by calling the claims department or submitting a claim form online. The insurance company will assign a claims adjuster to assist you with the process.

Required Documentation

To support your claim, you will need to provide documentation that proves the loss or damage. This may include:

- A detailed description of the incident, including the date, time, and location.

- Photographs or videos of the damage.

- Receipts or invoices for repairs or replacements.

- Medical records if there are injuries.

Timeline for Processing Claims

The timeline for processing claims can vary depending on the complexity of the case. However, the insurance company will typically aim to complete the investigation and make a decision within a reasonable timeframe.

If the claim is approved, the insurance company will issue a payment to cover the eligible expenses. If the claim is denied, the insurance company will provide a written explanation of the reasons for the denial.

Risk Management

Condo associations face various risks that can potentially lead to financial losses, property damage, or legal liabilities. Identifying and mitigating these risks is crucial for protecting the association’s assets and the well-being of its members.

To effectively manage risks, associations should implement comprehensive risk management plans that include the following elements:

Common Risks

Common risks that condo associations face include:

- Property damage from natural disasters, such as hurricanes, earthquakes, and fires.

- Liability claims due to injuries or accidents on common areas.

- Financial losses resulting from theft, fraud, or mismanagement.

- Cybersecurity breaches that compromise sensitive data or disrupt operations.

Risk Mitigation Strategies

Strategies for mitigating these risks include:

- Maintaining adequate insurance coverage to protect against property damage and liability claims.

- Implementing safety measures, such as security cameras, lighting, and fire alarms, to prevent accidents and injuries.

- Establishing sound financial policies and procedures to prevent fraud and mismanagement.

- Implementing cybersecurity measures, such as firewalls, intrusion detection systems, and data encryption, to protect against cyber threats.

Risk Management Plan

A comprehensive risk management plan should include the following steps:

- Identify and assess risks.

- Develop strategies to mitigate risks.

- Implement and monitor risk mitigation measures.

- Review and update the risk management plan regularly.

Board Responsibilities

The board of directors plays a crucial role in managing the master insurance policy. They are responsible for ensuring that the policy provides adequate coverage for the association and its members. This includes reviewing the policy regularly, working with insurance agents and brokers, and making sure that the association is meeting its insurance obligations.

Reviewing the Policy Regularly

The board should review the master insurance policy annually to make sure that it is still meeting the needs of the association. This review should include an assessment of the coverage limits, deductibles, and exclusions. The board should also make sure that the policy is up-to-date with any changes in the law or the association’s circumstances.

Working with Insurance Agents and Brokers

The board should work closely with insurance agents and brokers to obtain the best possible coverage for the association. The agent or broker can help the board understand the different types of coverage available, compare quotes from different insurance companies, and negotiate the best possible terms. The board should also make sure that the agent or broker is licensed and reputable.